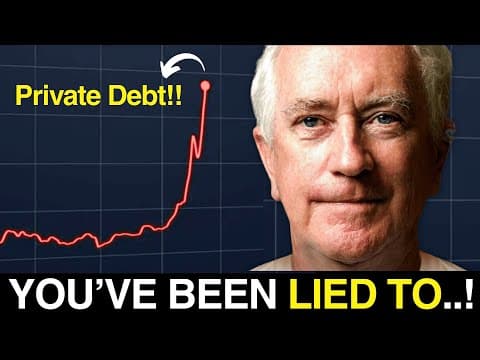

"Housing market is in its worst condition ever" Top Economist warns

Description

Learn 50+ Years of Economics in Only 7 Weeks: apply at https://www.stevekeen.com (Bonus: accepted students who join get Ravel — the double-entry, macro visualization tool used in this video.) Why are homes unaffordable from London to Sydney? Steve Keen shows why the standard “supply & demand” story misses the engine underneath modern housing bubbles: bank-originated mortgage credit. Using long-run BIS datasets, Steve tracks how real house prices decoupled from consumer prices after the 1980s as banks ramped mortgage lending. The kicker: it’s not just the level of mortgage debt that drives prices — it’s the change in the change of mortgage debt. That credit pulse explains booms, busts, and today’s squeeze. What you’ll learn • Why real house prices were flat for a century… then went vertical after the 1980s • How bank lending (not “savers’ deposits”) creates new purchasing power for housing • The critical driver: ΔΔ Mortgage Debt → Δ Real House Prices (UK, US, Australia, more) • Why simple correlations mislead — and why differencing reveals the true causal link • How rising inequality and speculative demand amplify bank-fueled price cycles • Policy levers that actually bite: credit guidance, LTV/DTI caps, and curbing mortgage speculation Key takeaways • Housing became a credit-fueled asset: prices outran CPI and wages because banks created the demand. • The credit impulse (change in the change of household debt) best explains house-price swings. • Countries without a visible “crash” can still be in an oversized, fragile credit cycle. • Taming bubbles means steering bank credit toward productive uses — not bidding wars for existing homes. Policy ideas discussed Credit guidance for banks: prioritize business working capital & durable goods; restrict mortgage speculation. Macroprudential limits: tighten LTV/DTI during upswings; countercyclical buffers that lean against credit booms. Re-align incentives: discourage flipping/empty-home speculation; reward new supply without turbo-charging land prices. Measure what matters: track private-debt ratios and the credit impulse alongside CPI/unemployment. ------ About Steve Keen Steve Keen builds accounting-consistent, data-driven models of money, debt, and instability. Creator of Minsky and Ravel, he replaces classroom myths with the operational mechanics you can simulate and test. Learn 50+ Years of Economics in Only 7 Weeks: apply at https://www.stevekeen.com (Bonus: accepted students who join get Ravel — the double-entry, macro visualization tool used in this video.) • Weekly live Q&A access • Cohort of rigorous learners • Ravel included for accepted students who join Support reality-based economics • Subscribe for more Ravel walk-throughs and housing myth-busting • Like if this reframed housing beyond “just build more” takes • Share with anyone who thinks deposits fund mortgages #housingcrisis #houseprices #mortgagedebt #CreditImpulse #PrivateDebt #BIS #Ravel #Macroeconomics #FinancialStability #Inequality #UKHousing #australiahousing #ushousingmarket #SteveKeen

Related Videos

”High-Cost debt is hammering Americans” Top Economist Warns

ProfSteveKeen

“Banks are HIDING something from us” Top Economist Warns

ProfSteveKeen

These 12 mins can CHANGE your view of classical economics

ProfSteveKeen

“Are you ready for this Once-in-a-Lifetime Crash?” Top Economist warns

ProfSteveKeen

“The real problem isn't deficits, It's Neoliberalism“ Top Economist warns

ProfSteveKeen

“Britain’s financial crisis no one is admitting” Top Economist Warns

ProfSteveKeen

“Why the US economy hasn’t crashed yet?” Top Economist warns

ProfSteveKeen

Top Economists: Don’t Study Economics! The textbooks taught us lies for 50 years

ProfSteveKeen

Is the UK heading into VERY dark times? Top Economist explains (with proof)

ProfSteveKeen

Australian housing crash 2025 explained: Top Economist warns

ProfSteveKeen

"TAX THE RICH" policy doesn't work alone: Top Economist

ProfSteveKeen

Ray Dalio and Mainstream are telling a lie: Top Economist warns

ProfSteveKeen