Why Your Investments Won’t Grow Like You Think

Jarrad Morrow

@jarradmorrowAbout

Want to invest smarter, spend with purpose, and retire on your terms? You’re in the right place. I’m Jarrad, a personal finance nerd who paid off $82K in debt, mastered budgeting, took a mini-retirement, and now saves/invests over 70% of my income on the path to Financial Independence. On this channel, I’ll teach you how to build wealth the simple, sustainable way through intentional spending, long-term investing, and taking full control of your money. If you’re ready to stop winging it and start building a future on your terms, subscribe and let’s get to work.

Latest Posts

Video Description

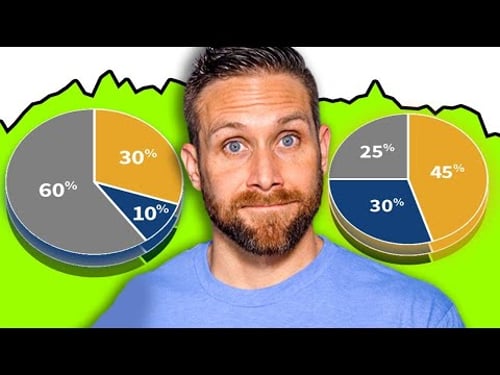

Check out My Recommendations (It helps support the channel): 📝 Boldin - The retirement planning tool I use to make sure I'm on track with saving for retirement. It's perfect for "Do it yourself" investors https://bit.ly/3EAAhrJ Personal Finance Bundle Wait List: https://bit.ly/4bpyTHT 📖 Free copy of my Spending Review Spreadsheet: https://bit.ly/48lMVZ1 📧 Business https://bit.ly/44AgfLw Assuming the wrong investment return can quietly derail your entire retirement plan. Overestimating future returns could leave you thousands behind your goals and force you to delay retirement. Underestimating them could lead you to over-save, sacrifice your lifestyle unnecessarily, and work longer than you actually need to. Even a small shift just 1% to 3% in your return assumption can swing your ending balance by hundreds of thousands of dollars. That’s why it’s crucial to use realistic return expectations when planning for retirement during the accumulation phase. Many people mistakenly run their numbers using historical averages like 12% per year, without adjusting for inflation. But those are nominal returns. The real return what actually matters for purchasing power has historically been closer to 9% after adjusting for inflation. And even that number smooths over the extreme volatility the market has delivered in the short and medium term. Rolling return data shows that over 10, 15, 20, and even 30 year periods, returns have varied widely from negative territory to well above average, depending entirely on when you invest. Using rolling period analysis, the data shows that 10-year returns ranged from 2% to 19%, while 30-year returns landed between 5% and 12%. While longer timeframes generally yield more consistent outcomes, the range of possible results makes it clear that no return assumption is guaranteed. Planning off the long term average without considering where the market is today especially in the context of high valuations can set false expectations. The smarter approach is to build your plan around a reasonable, slightly conservative real return assumption, such as 5%, 6%, or 7%, and test for a range of outcomes. This creates a buffer: if returns exceed expectations, you’re ahead. If they fall short, you’ve already accounted for it. More importantly, it's vital to adjust your plan over time and avoid the trap of "resulting," where people judge their financial decisions solely based on how things turned out rather than whether they were logical at the time. The key takeaway is that successful retirement planning isn’t about guessing the perfect return. It’s about using grounded assumptions, updating your plan regularly, and focusing on what you can control like savings rate, investment consistency, and managing costs so that you’re positioned to succeed regardless of what the market does. 00:00 The Future Investment Return Problem 00:36 When Numbers Lie 01:50 Paper Wealth vs. Real Life 04:08 The 100-Year Lie 05:38 How Decades Change the Game 08:33 The Smarter Way to Run the Numbers 12:04 The Poker Lesson for Retirement Affiliate Disclaimer: Some of the links above are affiliate links. If you sign up or make a purchase through them, I may earn a small commission at no extra cost to you. Your support means a lot and helps keep the channel going. Thank you! General Disclaimer: I am not a financial advisor and this video should not be taken as financial advice. This content is for entertainment and informational purposes only. Everyone’s financial situation is different, so be sure to do your own research and consider speaking with a professional before making any financial decisions. 285

You May Also Like

Investment Mastery Kit

AI-recommended products based on this video

The Book. The Ultimate Guide to Rebuilding a Civilization - Inspirational Science Books for Adults - Unique Artifact - Knowledge Encyclopedia with Over 400 Pages of Detailed & Catchy Illustrations

All the Way to the River: Oprah's Book Club: Love, Loss, and Liberation

Zhanmai Open When Envelopes for College Student, Going Away to College Gifts University Gift Card Book, High School Care Package, Birthday Cash Card Holder for Daughter Son Friends Gift(Pastel)